Setting the price of any product or service can certainly be overwhelming for any business owner. But the truth is that price is one of the most important elements of the marketing strategy (product, price, place and promotion), since it is the only factor that generates a return for the organization, and therefore impacts directly on the amount of profit made.

Pricing is a difficult task and it must always reflect the relationship between supply and demand. Furthermore, it should take the following into account:

- Fixed and variable costs

- Competition

- Company objectives

- Proposed positioning strategies

- Target group and willingness to pay

A company can choose from a great variety of pricing strategies depending on its aims and objectives. Some of the most widely used strategies are penetration pricing, premium pricing, competition pricing, cost-based pricing and value pricing.

In addition, there is a very specific strategy based on discounts and promotions, with which it is important to experiment, given that a small change in prices can have a big influence on sales. The first step in developing a better promotion strategy is segmenting the market into different groups, based on customers’ shopping preferences, for instance.

The main benefit of a discount pricing strategy lies in its ability to drive traffic and sales short term. However, this strategy should be used cautiously, for it might have some negative effects on market position and brand loyalty in the long run, or it could begin a downward pricing spiral that may eventually damage your ability to sell the product at full price.

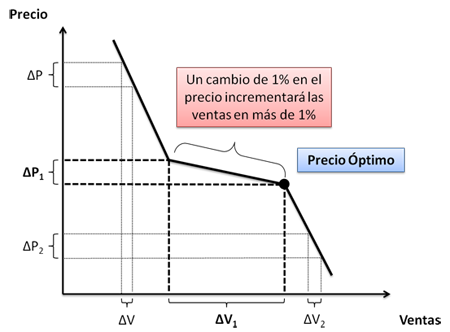

Price elasticity of demand is precisely a measure used to show the responsiveness of the quantity demanded of a product to a change in its price. Price elasticity models are handy tools in the development of pricing strategies, as they allow you to see the impact of a marginal change in price and they also evaluate how pricing can drive sales to support a business. In short, they attempt to express through a curve how much unit sales will increase or decrease if you raise or lower the price of your product by a small amount. Ideally, price elasticity models will help you determine the optimum price, or the price point after which a price drop by 1% will not allow volume increase by more than 1%.

PRICE ELASTICITY CHART

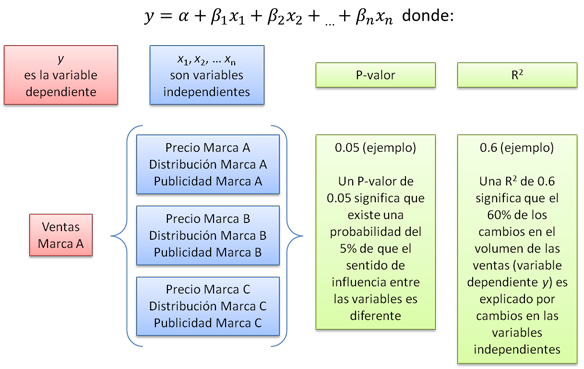

Some multi-variable regression models can analyze the impact on sales volume caused by changes in certain independent variables, such as price, distribution, and promotion activities of your company, as well as those of your competitors.

MULTI-VARIABLE REGRESSION MODEL

A very distinctive model is the Van Westendorp Price Sensitivity Model, in which price sensitivity relates not to absolute price, but rather to the perceived value of the good or service. Consumer price expectations and tolerances are measured by asking a set of price perception questions that are key to the model and the price at which the product or service is…

- So cheap that product quality/value is questionable (too inexpensive)

- A bargain (inexpensive)

- Beginning to seem too expensive (expensive)

- Too expensive to consider (too expensive/prohibitive)

The answers to these questions are then graphed and the Range of Acceptable Prices is defined. Consequently, the model allows us (as many other models do) to set a price that enables sales maximization and minimal loss in a world full of commodities, where competition is increasing by the day and product differentiation is becoming more difficult to establish.

References:

Photo by Pixabay on Pexels: https://www.pexels.com/photo/advertising-business-calculator-commercial-262470/